Dave Savastano, Editor03.09.15

While products in the flexible and printed electronics (PE) space cover a huge gamut of applications, they have certain elements in common. One of the common elements is the need for conductivity. PE applications ranging from sensors to solar, touch screens and displays to near field communication (NFC) and printed RFID tags and more utilize conductive materials.

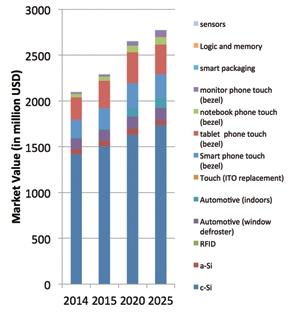

The market for conductive inks is booming. Dr. Khasha Ghaffarzadeh, head of consulting for IDTechEx, leading consultants in the field of printed and flexible electronics and organizers of the annual Printed Electronics USA, Europe and Asia conferences, said that the conductive ink and paste market will be $2.3 billion in 2015, and will continue to grow.

“This market is set to grow to nearly $3.2 billion in 2025, registering a CAGR of 3.26% over the decade,” Dr. Ghaffarzadeh said. “Conductive inks and pastes are used in a variety of application. The largest sector is photovoltaics (PV), in which conducting acts as printed bus bars. Membrane switches are also a prominent market, although it is a fragmented space in which there is little differentiation except price.

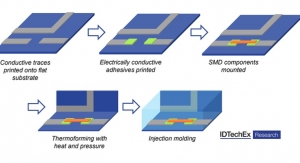

“Printing edge electrodes for touch screens is also a growing sector, although the tendency towards narrower bezels is a threat to screen printing while an opportunity for other forms of printing,” Dr. Ghaffarzadeh added. “Automotives, both in their interior and exterior, are also a large and growing sector. We note that the new emerging battlegrounds are applications such as electronic textiles, 3D printed electronics, thermoformed electronic objects, etc.”

“We see significant growth in many application areas, including displays, sensors, energy storage and flexible conductors such as antennas,” said Stan Farnsworth, VP of marketing for NovaCentrix, which has created leading technologies such as the PulseForge tools and Metalon inks. “Broader application types such as wearables, photovoltaics and automotive continue to see strong activity as well.”

Sun Chemical, the world’s largest printing ink manufacturer, has taken a lead role in the field of printed electronics. Roy Bjorlin, commercial director, Electronic Materials for Sun Chemical, reported that Sun Chemical is seeing growth in the flexible and printed electronics markets, with more PE applications reaching the pilot production and manufacturing stages.

“We continue to see growth in the flexible and printed electronics markets and our strategic focus continues to be on electronic packages or smart packages,” Bjorlin said. “We are certainly seeing more printed electronics applications reaching the pilot production and manufacturing stages. In particular, we are seeing the advanced designs moving towards production at a faster rate. This includes applications for nano silver and inkjet.”

Graphic courtesy of IDTechEx.

T+ink has developed more than 2,000 ink formulations for PE projects, including formulations for flexo, screen, inkjet, gravure and offset as well as coatings. Products designed by T+ink have appeared in markets ranging from toys and automotive parts to packaging and apparel and more. Its designers have partnered with major companies, including Ford, General Motors, McDonald’s, Coca-Cola and Wal-Mart.

John Gentile, president of T+ink, said there is real growth and high forecasted growth in the flexible electronics and packaging markets for PE.

“The technologies that win out to become ubiquitous will need to fit into existing equipment lines and run at traditional line speeds as well as being cost effective,” John Gentile added. “There are numerous technologies vying for adoption, but the winner will need to have a supply chain that is comfortable producing the printed electronics products with low fall out.

“T+ink has been in numerous pilots in 2013-2014, and the production actually starts this year for hundreds of millions of packages around the world,” John Gentile noted. “There is more coming as our technology achieves manufacturing status and adoption.”

As for key markets for conductive inks, Anthony Gentile, chief marketing officer for T+ink, noted that there are the traditional membrane and RFID markets, but they are mature to a degree with little technical innovation.

“We see more IME growth for capacitive switches for white goods, automotive and consumer electronics,” Anthony Gentile added. “We also see more authentication, security and customer interaction products being adopted that utilize our patented TouchCode technology.”

Dr. Allen Reid of NANOGAP said that he is seeing growth, but not as much as anticipated. “We manufacture conductive particles and sell to ink formulators, so we are one step away from end users,” Dr. Reid said. “However, we see growth in transparent conductive films for touch panels and for inkjet inks for printing on curved surfaces.”

“All of the oft-mentioned applications for printed electronics are current buyers of inks from NovaCentrix, with potential for volume growth,” Farnsworth said. “The difficult question to answer, however, is what types of volumes can each application reach? Some applications consume only small amounts of ink, and in fact customers are often engineering products to require as little ink as possible. From their perspective it makes sense: use as little as possible of a sometimes-expensive component material. Over time though, our expectation is that more and more products will utilize conductive inks as part of their embedded technology solution. For NovaCentrix, applications utilizing increasing quantities of conductive materials include RFID as well as displays.”

Consolidation and Alliances

There have been changes in the market, and collaborations and acquisitions have led to new opportunities.

“There has already been a mild and slow consolidation taking place amongst nanoparticle suppliers,” Dr. Ghaffarzadeh said. “For example, NovaCentrix acquired PChem Associates, Nanomas quietly left, Cabot stopped promoting its products, and Bayer sold its silver nanotech business to Clariant. The business scene was dominated by small suppliers, and most big players sat on the fence or just developed the technology in-house to hedge their bets.

“The industry is still characterized by a technology push, and go-to-market strategy is mostly one of substitution,” Dr. Ghaffarzadeh added. “This means that the pressure remains high, therefore the potential for further slow consolidation exists, although the supplier base is now narrower. In the conductive paste, part of the downturn in the PV sector negatively affected Ferro, which sold its business, mostly valued thanks to its IP assets, to Heraeus. This business scene remains populated with many large corporations, thus market entry for late entrants is challenging. The market pie is also large and growing.”

NovaCentrix purchased the nano silver-based flexo, spray and screen ink technology of PChem Associates in March 2014, and now offers its complete line of nano silver-based inks. Due to scaling efficiencies at NovaCentrix, the PChem inks are now available at reduced pricing.

“Legacy customers of PChem have told us they feel reassured in their use of PChem products given the stability of NovaCentrix as a long-term supplier,” Farnsworth noted. “New users of PChem products often discover these products through coming to our website or learning of them through any of the other promotional activities of NovaCentrix.”

In March 2014, Sun Chemical announced an alliance with T+ink called T+Sun. Sun Chemical brings manufacturing experience and extensive contacts with leading printers and brand owners.

From inception, T+Sun “hit the ground running,” said Ed Ickowski, T+ink’s EVP of sales. “The goal for T+Sun is to be the hub of the ecosystem.”

This collaboration is paying off with new opportunities for both companies as well as end users. T+ink’s TouchCode technology is one area in particular where the ability to communicate with consumers is enhancing the product experience.

“With a strategic focus on applications which include printed antenna RFID and 3D, smart labels, touch switches and sensors, and as part of our collaboration with T+ink, new advanced material packages for applications such as TouchCode, Sun Chemical has been exposed to significant opportunities where a new generation of materials is required,” Bjorlin said.

“Sun Chemical continues to be very focused on TouchCode, which represents a very significant bridge between print and digital in the packaging and label space, enabling a multitude of smart print solutions by connecting physical products to mobile devices,” Bjorlin added. “Our converter and brand owner partners are very enthusiastic. Beyond TouchCode we are working closely to develop a full stack of inks, from conductive inks to graphic inks, for in-mold applications where a membrane switch could become part of a 3-D design.”

Primary Materials for Conductive Inks

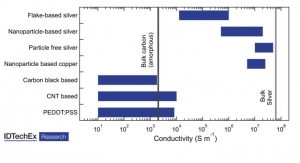

There are a wide range of materials being used for conductive inks. There are metal-based (silver and copper, to name two), carbon-based materials (graphite and carbon nanotubes) and nanoparticles of metals. Each of these materials offer their own distinct advantages.

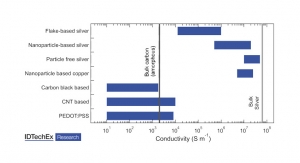

Dr. Ghaffarzadeh noted that silver is the most common metallic conductive ink, mainly because its oxide form also conducts. He added that copper and other silver alloys are also slowly emerging, although the main challenge is to anneal or sinter them without causing them to oxidize.

“Metallic inks and pastes can divided into two categories: (1) traditional micro-sized flakes and powders and (2) nano particle,” Dr. Ghaffarzadeh said. “The former is a mature technology that controls almost the entire market. The latter is an emerging option.

“Nanoparticles offer higher conductivity, which leads to less material consumption for the same conductance; better packing which leads to increased flexibility; and compatibility with inkjet printing,” Dr. Ghaffarzadeh added. “They have however been over-priced, meaning that they have had little success as substitutes. This is changing slowly as bigger players enter the market and a slow process of depreciation takes place.”

“PTF (polymer thick film) silver and carbon/graphite remain the dominant materials used in the market for conductive inks,” Bjorlin said. “However, nano silver inks are increasingly being developed for a number of applications. Sun Chemical has invested in a vertical integration, which includes synthesis, ink development and applications development.”

Farnsworth noted that silver continues to be the most prominent material used in conductive inks. “Silver can be utilized in many forms, including micron flakes, nanoparticles and organo-metallic formulations,” Farnsworth noted. “Silver nanowires are also being used now in the market. Silver is the material with the least adoption risk as far as technology, with some volatility though in the pricing of the silver raw materials.”

NovaCentrix is a leader in the field of copper-based conductive inks, and Farnsworth reported that NovaCentrix continues to advocate copper, including its own Metalon ICI inks.

“Originally debuting in 2009-2010, our current ICI ink formulations are more advanced than ever before, with excellent shelf stability and corrosion lifetimes,” Farnsworth said. “We also recently supported DuPont in the release of their new photonic copper ink at PE USA 2014 in Santa Clara, CA. Attendees could pick up printed samples of the DuPont ink at the DuPont booth, then bring it to the NovaCentrix exhibition area to be fully cured using our PulseForge photonic curing tools.”

Dr. Reid said that NANOGAP offers silver nanoparticles at high 70% wt. concentration for inkjet inks, providing long term stability, ease of formulating, high conductivity and low temperature sintering. NANOGAP’s silver nanofibers can be formulated into screen printing inks used to prepare transparent conductive films with good conductive and optical properties, suitable for use in printed lighting and photovoltaics.

Terry Kaiserman, chief technology officer for T+ink, noted that T+ink formulations cover almost the entire gamut of conductive materials as well as application methods.

“The advantage to these formulations are that they allow the printer to put the ink in their fountain or well and with a few tweaks, start printing and curing as they normally would,” Kaiserman said. “Each vehicle system is formulated to work on existing production lines.

“Solvent-based materials are used for screen, flexo, spray, dip coating, gravure, inkjet, slot die and other types of coating methods,” Kaiserman said. “Water-based materials are used for screen, inkjet, flexo, spray and coating methods. UV/EB materials are used in offset, screen, flexo and other coating methods. Oxidation ink types are used in offset predominantly.”

Kaiserman added that T+ink has a range of UV screen and flexo conductors that are being tested for a potential launch by mid-2015. This will be for both the company’s in mold patented process as well as standard TouchCode and security printed products.

Outlook for Flexible and Printed Electronics

Conductive ink manufacturers report that they are optimistic about the opportunities ahead for flexible and printed electronics.

“The outlook remains very bright for printed electronics,” Bjorlin said. “For Sun Chemical, the effort to support a full range of strategic applications has exposed us to many new growth opportunities. This has enabled our research teams to focus on developing new materials to support these emerging applications.”

Farnsworth said that NovaCentrix is seeing lots of growth. “The number of active and ongoing customer projects is growing, and the number of collaborations is growing,” Farnsworth added. “Every day we see more mainstream applications for flexible and printed electronics coming to us, with requests for product, process support and contracted development support.”

“We are on the cusp of incredible growth for printed electronics for the IoT market and wearables,” Kaiserman said. “T+ink’s origins have been in the printed electronics space since the early 1990s, and only now see the mass adoption and recognition that this field is the next high growth area that will change the world as we know it.”

The market for conductive inks is booming. Dr. Khasha Ghaffarzadeh, head of consulting for IDTechEx, leading consultants in the field of printed and flexible electronics and organizers of the annual Printed Electronics USA, Europe and Asia conferences, said that the conductive ink and paste market will be $2.3 billion in 2015, and will continue to grow.

“This market is set to grow to nearly $3.2 billion in 2025, registering a CAGR of 3.26% over the decade,” Dr. Ghaffarzadeh said. “Conductive inks and pastes are used in a variety of application. The largest sector is photovoltaics (PV), in which conducting acts as printed bus bars. Membrane switches are also a prominent market, although it is a fragmented space in which there is little differentiation except price.

“Printing edge electrodes for touch screens is also a growing sector, although the tendency towards narrower bezels is a threat to screen printing while an opportunity for other forms of printing,” Dr. Ghaffarzadeh added. “Automotives, both in their interior and exterior, are also a large and growing sector. We note that the new emerging battlegrounds are applications such as electronic textiles, 3D printed electronics, thermoformed electronic objects, etc.”

“We see significant growth in many application areas, including displays, sensors, energy storage and flexible conductors such as antennas,” said Stan Farnsworth, VP of marketing for NovaCentrix, which has created leading technologies such as the PulseForge tools and Metalon inks. “Broader application types such as wearables, photovoltaics and automotive continue to see strong activity as well.”

Sun Chemical, the world’s largest printing ink manufacturer, has taken a lead role in the field of printed electronics. Roy Bjorlin, commercial director, Electronic Materials for Sun Chemical, reported that Sun Chemical is seeing growth in the flexible and printed electronics markets, with more PE applications reaching the pilot production and manufacturing stages.

“We continue to see growth in the flexible and printed electronics markets and our strategic focus continues to be on electronic packages or smart packages,” Bjorlin said. “We are certainly seeing more printed electronics applications reaching the pilot production and manufacturing stages. In particular, we are seeing the advanced designs moving towards production at a faster rate. This includes applications for nano silver and inkjet.”

Graphic courtesy of IDTechEx.

John Gentile, president of T+ink, said there is real growth and high forecasted growth in the flexible electronics and packaging markets for PE.

“The technologies that win out to become ubiquitous will need to fit into existing equipment lines and run at traditional line speeds as well as being cost effective,” John Gentile added. “There are numerous technologies vying for adoption, but the winner will need to have a supply chain that is comfortable producing the printed electronics products with low fall out.

“T+ink has been in numerous pilots in 2013-2014, and the production actually starts this year for hundreds of millions of packages around the world,” John Gentile noted. “There is more coming as our technology achieves manufacturing status and adoption.”

As for key markets for conductive inks, Anthony Gentile, chief marketing officer for T+ink, noted that there are the traditional membrane and RFID markets, but they are mature to a degree with little technical innovation.

“We see more IME growth for capacitive switches for white goods, automotive and consumer electronics,” Anthony Gentile added. “We also see more authentication, security and customer interaction products being adopted that utilize our patented TouchCode technology.”

Dr. Allen Reid of NANOGAP said that he is seeing growth, but not as much as anticipated. “We manufacture conductive particles and sell to ink formulators, so we are one step away from end users,” Dr. Reid said. “However, we see growth in transparent conductive films for touch panels and for inkjet inks for printing on curved surfaces.”

“All of the oft-mentioned applications for printed electronics are current buyers of inks from NovaCentrix, with potential for volume growth,” Farnsworth said. “The difficult question to answer, however, is what types of volumes can each application reach? Some applications consume only small amounts of ink, and in fact customers are often engineering products to require as little ink as possible. From their perspective it makes sense: use as little as possible of a sometimes-expensive component material. Over time though, our expectation is that more and more products will utilize conductive inks as part of their embedded technology solution. For NovaCentrix, applications utilizing increasing quantities of conductive materials include RFID as well as displays.”

Consolidation and Alliances

There have been changes in the market, and collaborations and acquisitions have led to new opportunities.

“There has already been a mild and slow consolidation taking place amongst nanoparticle suppliers,” Dr. Ghaffarzadeh said. “For example, NovaCentrix acquired PChem Associates, Nanomas quietly left, Cabot stopped promoting its products, and Bayer sold its silver nanotech business to Clariant. The business scene was dominated by small suppliers, and most big players sat on the fence or just developed the technology in-house to hedge their bets.

“The industry is still characterized by a technology push, and go-to-market strategy is mostly one of substitution,” Dr. Ghaffarzadeh added. “This means that the pressure remains high, therefore the potential for further slow consolidation exists, although the supplier base is now narrower. In the conductive paste, part of the downturn in the PV sector negatively affected Ferro, which sold its business, mostly valued thanks to its IP assets, to Heraeus. This business scene remains populated with many large corporations, thus market entry for late entrants is challenging. The market pie is also large and growing.”

NovaCentrix purchased the nano silver-based flexo, spray and screen ink technology of PChem Associates in March 2014, and now offers its complete line of nano silver-based inks. Due to scaling efficiencies at NovaCentrix, the PChem inks are now available at reduced pricing.

“Legacy customers of PChem have told us they feel reassured in their use of PChem products given the stability of NovaCentrix as a long-term supplier,” Farnsworth noted. “New users of PChem products often discover these products through coming to our website or learning of them through any of the other promotional activities of NovaCentrix.”

In March 2014, Sun Chemical announced an alliance with T+ink called T+Sun. Sun Chemical brings manufacturing experience and extensive contacts with leading printers and brand owners.

From inception, T+Sun “hit the ground running,” said Ed Ickowski, T+ink’s EVP of sales. “The goal for T+Sun is to be the hub of the ecosystem.”

This collaboration is paying off with new opportunities for both companies as well as end users. T+ink’s TouchCode technology is one area in particular where the ability to communicate with consumers is enhancing the product experience.

“With a strategic focus on applications which include printed antenna RFID and 3D, smart labels, touch switches and sensors, and as part of our collaboration with T+ink, new advanced material packages for applications such as TouchCode, Sun Chemical has been exposed to significant opportunities where a new generation of materials is required,” Bjorlin said.

“Sun Chemical continues to be very focused on TouchCode, which represents a very significant bridge between print and digital in the packaging and label space, enabling a multitude of smart print solutions by connecting physical products to mobile devices,” Bjorlin added. “Our converter and brand owner partners are very enthusiastic. Beyond TouchCode we are working closely to develop a full stack of inks, from conductive inks to graphic inks, for in-mold applications where a membrane switch could become part of a 3-D design.”

Primary Materials for Conductive Inks

There are a wide range of materials being used for conductive inks. There are metal-based (silver and copper, to name two), carbon-based materials (graphite and carbon nanotubes) and nanoparticles of metals. Each of these materials offer their own distinct advantages.

Dr. Ghaffarzadeh noted that silver is the most common metallic conductive ink, mainly because its oxide form also conducts. He added that copper and other silver alloys are also slowly emerging, although the main challenge is to anneal or sinter them without causing them to oxidize.

“Metallic inks and pastes can divided into two categories: (1) traditional micro-sized flakes and powders and (2) nano particle,” Dr. Ghaffarzadeh said. “The former is a mature technology that controls almost the entire market. The latter is an emerging option.

“Nanoparticles offer higher conductivity, which leads to less material consumption for the same conductance; better packing which leads to increased flexibility; and compatibility with inkjet printing,” Dr. Ghaffarzadeh added. “They have however been over-priced, meaning that they have had little success as substitutes. This is changing slowly as bigger players enter the market and a slow process of depreciation takes place.”

“PTF (polymer thick film) silver and carbon/graphite remain the dominant materials used in the market for conductive inks,” Bjorlin said. “However, nano silver inks are increasingly being developed for a number of applications. Sun Chemical has invested in a vertical integration, which includes synthesis, ink development and applications development.”

Farnsworth noted that silver continues to be the most prominent material used in conductive inks. “Silver can be utilized in many forms, including micron flakes, nanoparticles and organo-metallic formulations,” Farnsworth noted. “Silver nanowires are also being used now in the market. Silver is the material with the least adoption risk as far as technology, with some volatility though in the pricing of the silver raw materials.”

NovaCentrix is a leader in the field of copper-based conductive inks, and Farnsworth reported that NovaCentrix continues to advocate copper, including its own Metalon ICI inks.

“Originally debuting in 2009-2010, our current ICI ink formulations are more advanced than ever before, with excellent shelf stability and corrosion lifetimes,” Farnsworth said. “We also recently supported DuPont in the release of their new photonic copper ink at PE USA 2014 in Santa Clara, CA. Attendees could pick up printed samples of the DuPont ink at the DuPont booth, then bring it to the NovaCentrix exhibition area to be fully cured using our PulseForge photonic curing tools.”

Dr. Reid said that NANOGAP offers silver nanoparticles at high 70% wt. concentration for inkjet inks, providing long term stability, ease of formulating, high conductivity and low temperature sintering. NANOGAP’s silver nanofibers can be formulated into screen printing inks used to prepare transparent conductive films with good conductive and optical properties, suitable for use in printed lighting and photovoltaics.

Terry Kaiserman, chief technology officer for T+ink, noted that T+ink formulations cover almost the entire gamut of conductive materials as well as application methods.

“The advantage to these formulations are that they allow the printer to put the ink in their fountain or well and with a few tweaks, start printing and curing as they normally would,” Kaiserman said. “Each vehicle system is formulated to work on existing production lines.

“Solvent-based materials are used for screen, flexo, spray, dip coating, gravure, inkjet, slot die and other types of coating methods,” Kaiserman said. “Water-based materials are used for screen, inkjet, flexo, spray and coating methods. UV/EB materials are used in offset, screen, flexo and other coating methods. Oxidation ink types are used in offset predominantly.”

Kaiserman added that T+ink has a range of UV screen and flexo conductors that are being tested for a potential launch by mid-2015. This will be for both the company’s in mold patented process as well as standard TouchCode and security printed products.

Outlook for Flexible and Printed Electronics

Conductive ink manufacturers report that they are optimistic about the opportunities ahead for flexible and printed electronics.

“The outlook remains very bright for printed electronics,” Bjorlin said. “For Sun Chemical, the effort to support a full range of strategic applications has exposed us to many new growth opportunities. This has enabled our research teams to focus on developing new materials to support these emerging applications.”

Farnsworth said that NovaCentrix is seeing lots of growth. “The number of active and ongoing customer projects is growing, and the number of collaborations is growing,” Farnsworth added. “Every day we see more mainstream applications for flexible and printed electronics coming to us, with requests for product, process support and contracted development support.”

“We are on the cusp of incredible growth for printed electronics for the IoT market and wearables,” Kaiserman said. “T+ink’s origins have been in the printed electronics space since the early 1990s, and only now see the mass adoption and recognition that this field is the next high growth area that will change the world as we know it.”