Dr. Tony Tianyi Sun, Lux Research Analyst12.01.15

Electronic consumer device innovation has typically run hand in hand with innovation in the displays they carry. A case in point is the emergence of liquid crystal displays (LCDs) from early adoption in laptops to become the leading display technology in almost all of today’s applications.

However, a new generation of devices – namely wearable and flexible devices – has highlighted LCDs’ limitations in visual performance, power consumption and rigidity, thereby enabling market opportunities for a new generation of display technologies and a proliferation of form factors and use cases.

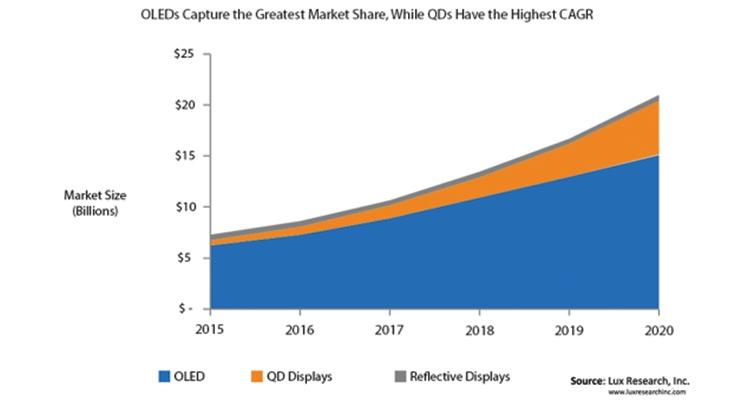

Three technologies stand out as the battle for market dominance ensues: organic light-emitting diode (OLEDs), reflective displays and the quantum dot (QD) backlight enhancement technology. As a group, these will grow at a compound annual growth rate (CAGR) of 24% to $21 billion in 2020, up from today’s $7.3 billion. However, not all of these technologies will find the same success.

OLEDs will grow into a $15 billion market in 2020, up from $6.2 billion in 2015, corresponding to a CAGR of 19%. Smartphones are the leading market due to superior visual performance and form factors. However, OLED’s wider adoption is limited by issues like differential aging and high cost in large formats, which limits the large addressable market of TVs only reaching $480 million in 2020.

QD LCDs represent the highest CAGR among emerging displays at 60%, although from the lowest base of the three technologies of $510 million in 2015. This will balloon to $5.3 billion in 2020, corresponding to an opportunity of $500 million for QD enhancement components. TVs will drive the QD LCD, comprising 96% of the total.

Finally, reflective displays will grow to $590 million in 2020, only $30 million more than today’s $560 million. An anticipated 40% decline in the e-reader market is a hole to fill, but emerging applications like signage, electronic shelf labels and wearables will indeed fill that gap with a little left over. Electrophoretic displays (EPDs) dominate the current reflective display market, but alternative reflective technologies – namely cholesteric LCDs (Ch-LCDs) and memory LCDs – will find opportunities from signage and wearables respectively.

And for those looking for growth in microelectromechanical systems (MEMS) and electrowetting (EW) displays; well, there’s still a lot of technical improvement required to be market-ready by 2020.

What is clear is that there won’t be a single display dominating all applications. While OLEDs, QD LCDs and reflective displays can compete with LCDs and garner significant market share, the overall display industry will fragment in the coming years, with different technologies gaining favor in different segments.

Because different display technologies have very different architectures, to maximize revenue and keep on track with display advancement, chemical and material developers need to diversify their product portfolio to fit individual technologies’ needs. Display developers also need to broaden their scope as today’s displays incorporate more functions, including sensors and haptics, to become the central piece for communication between human and electronics devices.

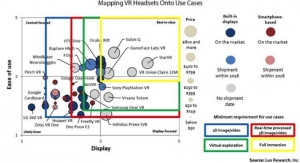

To keep pace, display developers need to proactively take expandability and integration with new input/output technologies into consideration for future success. Of course, disruption and opportunity won’t stop with the tactile user interfaces. The way people perceive or process images is on the technology roadmap, with augmented reality headsets in the near-term solution, and futuristic eye-hacking by neuroscience technologies emerging from the cutting edge, forcing developers to think about displays differently.

Whatever part of the display value chain you care about, change is most certainly coming, moving existing markets and creating entirely new ones.

Tony Sun is an analyst on the Wearable and Flexible Electronics Intelligence team at Lux Research, which provides strategic advice and on-going intelligence for emerging technologies. He holds an M.S. and Ph.D. in physics from Boston College and obtained his B.S. in physics from Peking University in Beijing, China. For more information, visit Lux Research.

However, a new generation of devices – namely wearable and flexible devices – has highlighted LCDs’ limitations in visual performance, power consumption and rigidity, thereby enabling market opportunities for a new generation of display technologies and a proliferation of form factors and use cases.

Three technologies stand out as the battle for market dominance ensues: organic light-emitting diode (OLEDs), reflective displays and the quantum dot (QD) backlight enhancement technology. As a group, these will grow at a compound annual growth rate (CAGR) of 24% to $21 billion in 2020, up from today’s $7.3 billion. However, not all of these technologies will find the same success.

OLEDs will grow into a $15 billion market in 2020, up from $6.2 billion in 2015, corresponding to a CAGR of 19%. Smartphones are the leading market due to superior visual performance and form factors. However, OLED’s wider adoption is limited by issues like differential aging and high cost in large formats, which limits the large addressable market of TVs only reaching $480 million in 2020.

QD LCDs represent the highest CAGR among emerging displays at 60%, although from the lowest base of the three technologies of $510 million in 2015. This will balloon to $5.3 billion in 2020, corresponding to an opportunity of $500 million for QD enhancement components. TVs will drive the QD LCD, comprising 96% of the total.

Finally, reflective displays will grow to $590 million in 2020, only $30 million more than today’s $560 million. An anticipated 40% decline in the e-reader market is a hole to fill, but emerging applications like signage, electronic shelf labels and wearables will indeed fill that gap with a little left over. Electrophoretic displays (EPDs) dominate the current reflective display market, but alternative reflective technologies – namely cholesteric LCDs (Ch-LCDs) and memory LCDs – will find opportunities from signage and wearables respectively.

And for those looking for growth in microelectromechanical systems (MEMS) and electrowetting (EW) displays; well, there’s still a lot of technical improvement required to be market-ready by 2020.

What is clear is that there won’t be a single display dominating all applications. While OLEDs, QD LCDs and reflective displays can compete with LCDs and garner significant market share, the overall display industry will fragment in the coming years, with different technologies gaining favor in different segments.

Because different display technologies have very different architectures, to maximize revenue and keep on track with display advancement, chemical and material developers need to diversify their product portfolio to fit individual technologies’ needs. Display developers also need to broaden their scope as today’s displays incorporate more functions, including sensors and haptics, to become the central piece for communication between human and electronics devices.

To keep pace, display developers need to proactively take expandability and integration with new input/output technologies into consideration for future success. Of course, disruption and opportunity won’t stop with the tactile user interfaces. The way people perceive or process images is on the technology roadmap, with augmented reality headsets in the near-term solution, and futuristic eye-hacking by neuroscience technologies emerging from the cutting edge, forcing developers to think about displays differently.

Whatever part of the display value chain you care about, change is most certainly coming, moving existing markets and creating entirely new ones.

Tony Sun is an analyst on the Wearable and Flexible Electronics Intelligence team at Lux Research, which provides strategic advice and on-going intelligence for emerging technologies. He holds an M.S. and Ph.D. in physics from Boston College and obtained his B.S. in physics from Peking University in Beijing, China. For more information, visit Lux Research.